#Telecom Power System Market Share

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has 16.74 million mobile monthly users in the US.

Text

Navigating the Telecom Power System Market: Global Industry Outlook

Increasing demand for compact and modular telecom power systems and the growing adoption of virtualization in telecom power systems are likely to drive the Market in the forecast period.

According to TechSci Research report, “Telecom Power System Market – Global Industry Size, Share, Trends, Competition Forecast & Opportunities, 2028”, the Global Telecom Power System Market is experiencing a surge in demand in the forecast period. A primary driver propelling the global Telecom Power System market is the widespread deployment of 5G technology. The advent of 5G has ushered in a new era of connectivity, offering faster data speeds, reduced latency, and increased network capacity. The implementation of 5G networks requires a significant upgrade of telecom infrastructure, driving the demand for advanced Telecom Power Systems. These systems play a pivotal role in providing the reliable and efficient power necessary to support the denser network of small cells characteristic of 5G deployment.

Telecom Power Systems must adapt to the unique requirements of 5G, accommodating the increased number of small cells and ensuring seamless integration into diverse environments. As the global demand for higher data speeds and enhanced connectivity continues to grow, the deployment of 5G technology acts as a potent driver, pushing the Telecom Power System market to innovate and evolve to meet the challenges of this next-generation network.

The exponential growth of the Internet of Things (IoT) is a significant driver fueling the global Telecom Power System market. The increasing prevalence of connected devices, from smart sensors to industrial machinery, demands a robust and reliable telecommunication infrastructure. Telecom Power Systems play a critical role in supporting the communication needs of IoT applications, providing the necessary power to base stations and data centers.

As industries across sectors embrace IoT for improved efficiency and real-time monitoring, the demand for Telecom Power Systems that can handle the unique challenges posed by IoT deployments is on the rise. These power systems must be scalable, energy-efficient, and capable of adapting to the diverse needs of IoT, contributing to the seamless integration and functionality of connected devices. The proliferation of IoT applications worldwide acts as a driving force, compelling Telecom Power System providers to develop innovative solutions to meet the evolving demands of this interconnected era.

Browse over XX Market data Figures spread through XX Pages and an in-depth TOC on "Global Telecom Power System Market.” https://www.techsciresearch.com/report/telecom-power-system-market/23070.html

The Global Telecom Power System Market is segmented into grid type, component, power source, and region.

Based on grid type, The On Grid segment held the largest Market share in 2022. On-Grid systems are well-suited for urban and developed areas where the power grid infrastructure is stable and reliable. In these regions, there is a consistent and uninterrupted power supply, making on-grid solutions a cost-effective and practical choice.

Connecting telecom infrastructure to an existing power grid is often more cost-effective than setting up independent power systems. The infrastructure is already in place, reducing the need for additional investment in off-grid or backup power solutions.

On-Grid systems benefit from the reliability and consistency of power supply from the main electrical grid. Telecom operations in areas with a stable grid connection experience minimal disruptions, ensuring continuous communication services.

Maintenance and servicing of on-grid power systems are generally more straightforward. The infrastructure is readily accessible, and any issues can be addressed without the complexity associated with off-grid solutions, where remote locations may pose logistical challenges.

In regions where the cost of energy from the grid is competitive or economical, telecom operators may opt for on-grid solutions. The availability of affordable grid electricity can make on-grid Telecom Power Systems a financially viable choice.

Regulatory frameworks and permitting processes often favor on-grid solutions, especially in urban areas. Connecting to the existing power grid may involve fewer regulatory hurdles compared to establishing off-grid or hybrid solutions with renewable energy sources.

On-Grid systems offer scalability, allowing telecom operators to easily expand their networks without significant modifications to the power infrastructure. This scalability is particularly beneficial in densely populated urban areas experiencing high demand for telecommunication services.

Based on power source, The diesel-Battery segment held the largest Market share in 2022. Diesel generators are known for their reliability and can provide a constant power supply. This is crucial for telecom infrastructure, where uninterrupted power is essential to ensure continuous communication.

Diesel generators can operate in various environmental conditions, making them suitable for telecom installations in diverse locations, including remote or challenging terrains.

Diesel generators can operate for extended periods without refueling, providing an autonomous power source. This is particularly important in areas with unreliable or no access to the electrical grid.

Combining diesel generators with battery systems allows for better energy management. Batteries can store excess energy generated by the diesel generator and release it during peak demand or in case of generator failure, providing a seamless power supply.

Modern diesel generators are designed to be fuel-efficient, reducing operational costs over time. The combination of diesel and battery systems allows for optimization of fuel usage.

While diesel generators are known for their emissions, advancements in technology have led to more fuel-efficient and environmentally friendly models. Additionally, the integration of battery systems helps reduce reliance on diesel power during periods of lower demand.

In regions with unreliable or underdeveloped power grids, telecom installations often need to operate independently. Diesel-battery systems provide a reliable off-grid solution.

Major companies operating in the Global Telecom Power System Market are:

Huawei Technologies Co., Ltd.

Ericsson AB

Nokia Corporation

ABB Ltd.

Emerson Electric Co.

Siemens AG

Eaton Corporation PLC

Schneider Electric SE

Hitachi Ltd.

Samsung Electronics Co., Ltd.

Download Free Sample Report https://www.techsciresearch.com/sample-report.aspx?cid=23070

Customers can also request for 10% free customization on this report.

“The Global Telecom Power System Market is expected to rise in the upcoming years and register a significant CAGR during the forecast period. The growth of the telecom power systems market is being driven by several factors, including the increasing demand for reliable and efficient power systems for telecommunications networks, the growing adoption of 5G networks, and the increasing need for renewable energy sources. Also, The Asia Pacific region is expected to be the fastest-growing market for telecom power systems, due to the rapid growth of the telecommunications industry in the region.

The Middle East and Africa region is also expected to witness significant growth, as countries in the region invest in upgrading their telecommunications infrastructure. The telecom power systems market is a fragmented market, with a large number of players. Some of the leading players in the market include Huawei, Ericsson, Nokia, ABB, and Emerson Electric. Therefore, the Market of Telecom Power System is expected to boost in the upcoming years.,” said Mr. Karan Chechi, Research Director with TechSci Research, a research-based management consulting firm.

“Telecom Power System Market - Global Industry Size, Share, Trends, Opportunity, and Forecast, 2018-2028 Segmented By Grid Type (On Grid, Off Grid, Bad Grid), By Component (Rectifier, Inverter, Converter, Controller, Heat Management Systems, Generators, Others), By Power Source (Diesel-Battery, Diesel-Solar, Diesel-Wind, Multiple Sources), By Region, By Competition”, has evaluated the future growth potential of Global Telecom Power System Market and provides statistics & information on Market size, structure and future Market growth. The report intends to provide cutting-edge Market intelligence and help decision-makers make sound investment decisions., The report also identifies and analyzes the emerging trends along with essential drivers, challenges, and opportunities in the Global Telecom Power System Market.

Browse Related Reports

Air-Operated Grease Market https://www.techsciresearch.com/report/air-operated-grease-market/23568.html

Portable Grease Pumps Market https://www.techsciresearch.com/report/portable-grease-pumps-market/23569.html

Industrial Belt Drives Market https://www.techsciresearch.com/report/industrial-belt-drives-market/23573.html Contact Us-

TechSci Research LLC

420 Lexington Avenue, Suite 300,

New York, United States- 10170

M: +13322586602

Email: [email protected]

Website: www.techsciresearch.com

#Telecom Power System Market#Telecom Power System Market Size#Telecom Power System Market Share#Telecom Power System Market Trends#Telecom Power System Market Growth

0 notes

Text

Exploring the Growth and Opportunities in the Telecom Tower Power Systems Market

The Telecom Tower Power Systems Market is witnessing significant growth, driven by the rising demand for seamless connectivity, increased mobile data traffic, and the expansion of telecom infrastructure in remote and rural areas. As the telecom industry rapidly evolves to support 5G technology, the need for robust and efficient power systems becomes increasingly critical. This market is poised…

#Telecom Tower Power Systems Market#Telecom Tower Power Systems Market Demand#Telecom Tower Power Systems Market Forecast#Telecom Tower Power Systems Market Growth#Telecom Tower Power Systems Market Report#Telecom Tower Power Systems Market Share#Telecom Tower Power Systems Market Size#Telecom Tower Power Systems Market Trends

0 notes

Text

The global telecom power systems market size reached US$ 5.3 Billion in 2023. Looking forward, IMARC Group expects the market to reach US$ 10.5 Billion by 2032, exhibiting a growth rate (CAGR) of 7.7% during 2024-2032.

#telecom power systems market#telecom power systems market size#telecom power systems market share#telecom power systems market demand#telecom power systems market report

0 notes

Text

Telecom Power Systems Market Size, Demand, Top Companies and Forecast 2023-2028

IMARC Group has recently released a new research study titled “Telecom Power Systems Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2023-2028”, offers a detailed analysis of the market drivers, segmentation, growth opportunities, trends and competitive landscape to understand the current and future market scenarios. How big is the telecom power systems market? The…

View On WordPress

#Telecom Power Systems Market#Telecom Power Systems Market Report#Telecom Power Systems Market Share

0 notes

Text

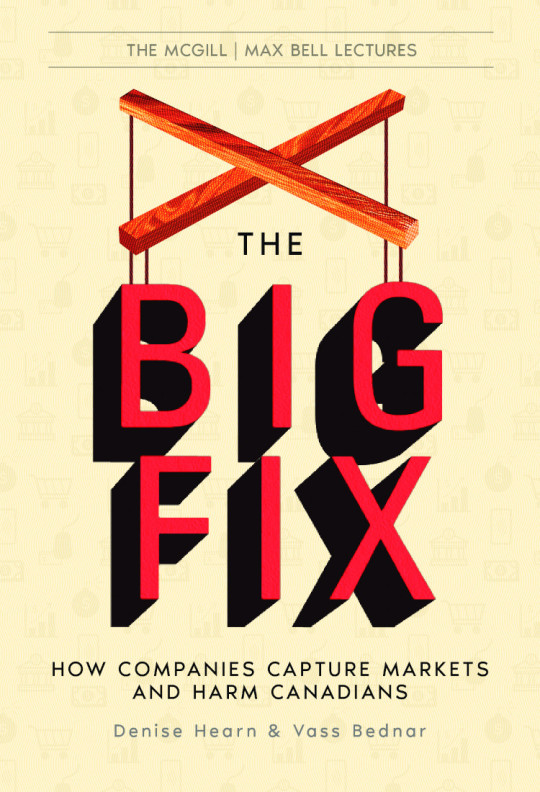

Denise Hearn and Vass Bednar’s “The Big Fix”

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2024/12/05/ted-rogers-is-a-dope/#galen-weston-is-even-worse

The Canadian national identity involves a lot of sneering at the US, but when it comes to oligarchy, Canada makes America look positively amateurish.

If you'd like an essay-formatted version of this thread to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2024/12/05/ted-rogers-is-a-dope/#galen-weston-is-even-worse

Canada's monopolists may be big fish in a small pond, but holy moly are they big, compared to the size of that pond. In their new book, The Big Fix: How Companies Capture Markets and Harm Canadians, Denise Hearn and Vass Bednar lay bare the price-gouging, policy-corrupting ripoff machines that run the Great White North:

https://sutherlandhousebooks.com/product/the-big-fix/

From telecoms to groceries to pharmacies to the resource sector, Canada is a playground for a handful of supremely powerful men from dynastic families, who have bought their way to dominance, consuming small businesses by the hundreds and periodically merging with one another.

Hearn and Bednar tell this story and explain all the ways that Canadian firms use their market power to reduce quality, raise prices, abuse workers and starve suppliers, even as they capture the government and the regulators who are supposed to be overseeing them.

The odd thing is that Canada has been in the antitrust game for a long time: Canada passed its first antitrust law in 1889, a year before the USA got around to inaugurating its trustbusting era with the passage of the Sherman Act. But despite this early start, Canada's ultra-rich have successfully used the threat of American corporate juggernauts to defend the idea of Made-in-Canada monopolies, as homegrown King Kongs that will keep the nation safe from Yankee Godzillas.

Canada's Competition Bureau is underfunded and underpowered. In its entire history, the agency has never prevented a merger – not even once. This set the stage for Canada's dominant businesses to become many-tentacled conglomerates, like Canadian Tire, which owns Mark's Work Warehouse, Helly Hansen, SportChek, Nevada Bob's Golf, The Fitness Source, Party City, and, of course, a bank.

A surprising number of Canadian conglomerates end up turning into banks: Loblaw has a bank. So does Rogers. Why do these corrupt, price-gouging companies all go into "financial services?" As Hearn and Bednar explain, owning a bank is the key to financialization, with the company's finances disappearing into a black box that absorbs taxation attempts and liabilities like a black hole eating a solar system.

Of course, the neat packaging up of vast swathes of Canada's economy into these financialized and inscrutable mega-firms makes them awfully convenient acquisition targets for US and offshore private equity firms. When the Competition Bureau (inevitably) fails to block those acquisitions, whole chunks of the Canadian economy disappear into foreign hands.

This is a short book, but it's packed with a lot of easily digested detail about how these scams work: how monopolies use cross-subsidies (when one profitable business is used to prop up an unprofitable business in order to kill potential competitors) and market power to rip Canadians off and screw workers.

But the title of the book is The Big Fix, so it's not all doom and gloom. Hearn and Bednar note that Canadians and their elected reps are getting sick of this shit, and a bill to substantially beefed up Canadian competition law passed Parliament unanimously last year.

This is part of a wave of antitrust fever that's sweeping the world's governments, notably the US under Biden, where antitrust enforcers did more in the past four years than their predecessors accomplished over the previous 40 years.

Hearn and Bednar propose a follow-on agenda for Canadian lawmakers and bureaucrats: they call for a "whole of government" approach to dismantling Canada's monopolies, whereby each ministry would be charged with combing through its enabling legislation to find latent powers that could be mobilized against monopolies, and then using those powers.

The authors freely admit that this is an American import, modeled on Biden's July 2021 Executive Order on monopolies, which set out 72 action items for different parts of the administration, virtually all of which were accomplished:

https://www.eff.org/deeplinks/2021/08/party-its-1979-og-antitrust-back-baby

What the authors don't mention is that this plan was actually cooked up by a Canadian: Columbia law professor Tim Wu, who served in the White House as Biden's tech antitrust czar, and who grew up in Toronto (we've known each other since elementary school!).

Wu's plan has been field tested. It worked. It was exciting and effective. There's something weirdly fitting about finding the answer to Canada's monopoly problems coming from America, but only because a Canadian had to go there to find a receptive audience for it.

The Big Fix is a fantastic primer on the uniquely Canadian monopoly problem, a fast read that transcends being a mere economics primer or history lesson. It's a book that will fire you up, make you angry, make you determined, and explain what comes next.

161 notes

·

View notes

Text

Back Office Workforce Management Market Size, Share & Growth Analysis 2034: Optimizing Operations with Automation & AI

Back Office Workforce Management Market is rapidly evolving as organizations seek smarter ways to handle non-customer-facing operations. Encompassing solutions such as task scheduling, labor forecasting, performance analytics, and time and attendance systems, this market is pivotal for businesses striving to increase operational efficiency. From banking to retail, companies are turning to these tools to automate manual processes, manage human capital effectively, and support strategic decision-making. With a market value of $3.1 billion in 2024 and projected growth to $6.4 billion by 2034, the sector is gaining strong momentum with a healthy CAGR of 7.5%.

Market Dynamics

What’s fueling this growth is a mix of technological innovation, rising labor costs, and the growing demand for transparency and accountability in business operations. The cloud-based deployment model leads with a 45% market share, offering flexibility, real-time access, and scalability to enterprises of all sizes. This is followed by on-premise (30%) and hybrid (25%) solutions, each addressing unique organizational needs.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS24564

The top-performing sub-segment is scheduling and forecasting, as organizations seek accurate, automated methods to deploy resources more efficiently. Close behind is analytics and reporting, where businesses are capitalizing on real-time data to fine-tune productivity and performance. As hybrid and remote work become the norm, solutions that support workforce visibility and self-service functionality are in high demand.

Key Players Analysis

Major players such as Verint Systems, NICE Systems, and Aspect Software are leading the charge with robust platforms that integrate AI, machine learning, and mobile capabilities. These companies continue to innovate, delivering tools that not only optimize task assignments but also offer insights into workforce trends and operational gaps.

Emerging players like Work Sync Innovations, Back Office Dynamics, and Efficient Ops are also disrupting the space. Their agility in customizing niche solutions for SMEs and specific industries such as healthcare or retail makes them strong contenders. A common thread among these players is a focus on subscription-based models and user-friendly interfaces, making their platforms more accessible and cost-effective.

Regional Analysis

North America holds the dominant position in the back office workforce management market. The United States, with its strong presence of large enterprises and advanced tech infrastructure, drives innovation and adoption. Cloud-based tools and AI-powered platforms are becoming staples in sectors such as finance and telecom.

Europe follows closely, where compliance with labor laws and a structured approach to workforce efficiency have spurred adoption. Countries like Germany, France, and the UK are investing in data-driven performance tracking systems, particularly in industrial and government sectors.

The Asia Pacific region is emerging as a growth hub, thanks to the expanding service sector in India, China, and Southeast Asia. Digital transformation, coupled with a rising middle class and rapid urbanization, is accelerating demand for scalable workforce solutions.

Latin America and the Middle East & Africa are showing promising signs of adoption as businesses in these regions move toward operational maturity. Government support for digital infrastructure and increasing awareness of workforce optimization benefits are contributing to gradual but steady market penetration.

Recent News & Developments

The integration of AI and machine learning has revolutionized forecasting and performance analytics in workforce management. These technologies enable predictive insights, helping organizations proactively manage staffing, avoid bottlenecks, and ensure regulatory compliance. Companies like NICE Systems have introduced intelligent platforms that analyze employee behavior, forecast workloads, and generate actionable strategies in real time.

Another significant trend is the rise of subscription-based pricing models, which provide flexibility for smaller businesses to access enterprise-grade solutions. Additionally, cloud adoption continues to rise, enhancing real-time collaboration and mobility — a must-have in today’s hybrid working world.

Recent product launches and strategic partnerships between software vendors and system integrators are shaping the competitive landscape. These developments aim to deliver more integrated, customizable, and mobile-friendly platforms, especially for industries undergoing rapid digital shifts like retail, education, and healthcare.

Browse Full Report : https://www.globalinsightservices.com/reports/back-office-workforce-management-market/

Scope of the Report

This report presents a comprehensive overview of the Back Office Workforce Management Market, analyzing trends, opportunities, and challenges across types, applications, technologies, and regions. It covers historical data from 2018 to 2023, with forecasts up to 2034, providing businesses with deep insights into market growth and technological advancements.

Key areas explored include cloud versus on-premise deployments, AI integration, regulatory compliance strategies, and emerging use cases in hybrid work environments. The report also profiles key and emerging players, offering competitive intelligence on mergers, partnerships, and innovation strategies shaping the future of back office management.

#workforcemanagement #backofficeautomation #cloudsolutions #remoteworktools #aibusinesssolutions #digitaltransformation #employeeefficiency #hybridworktech #taskoptimization #enterprisetechnology

Discover Additional Market Insights from Global Insight Services:

Commercial Drone Market : https://www.globalinsightservices.com/reports/commercial-drone-market/

Product Analytics Market : https://www.globalinsightservices.com/reports/product-analytics-market/

Streaming Analytics Market : https://www.globalinsightservices.com/reports/streaming-analytics-market/

Cloud Native Storage Market ; https://www.globalinsightservices.com/reports/cloud-native-storage-market/

Alternative Lending Platform Market : https://www.globalinsightservices.com/reports/alternative-lending-platform-market/

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

Global SOFC Market to Reach Multibillion-Dollar Milestone by 2030

Solid Oxide Fuel Cell Market Set for Multi-Billion Dollar Expansion by 2030, Driven by Clean Energy Demand and Fuel Flexibility

The solid oxide fuel cell (SOFC) market is undergoing unprecedented growth as global demand for cleaner, more resilient energy solutions intensifies. Valued at around USD 3.0 billion in 2024, the market is projected to expand at a compound annual growth rate (CAGR) of 26% to 30% over the next decade, reaching over USD 20 billion by 2032. The surge is fueled by increasing adoption across stationary power systems, the push for hydrogen-based energy, and major investments in fuel cell technologies from leading economies like the United States and Japan.

To Get Free Sample Report : https://www.datamintelligence.com/download-sample/solid-oxide-fuel-cell-market

Key Market Drivers

1. Clean Energy and Decarbonization Goals SOFCs generate electricity with high efficiency and low emissions by using fuels like hydrogen, natural gas, or biogas. Their ability to produce power at efficiencies above 60% and over 80% when used in combined heat and power (CHP) configurations makes them attractive for industrial, commercial, and residential applications aiming to reduce carbon footprints.

2. Government Policy and Incentives Supportive energy policies are a primary catalyst for SOFC adoption. In the United States, federal energy departments are investing heavily in SOFC R&D and pilot projects for defense, data centers, and critical infrastructure. Japan's Green Growth Strategy promotes widespread use of SOFCs in residential and commercial sectors. These programs are accelerating commercialization and technological maturity.

3. Advancements in Materials and Stack Design Recent breakthroughs in ceramic electrolytes, anode-supported cells, and metal-supported stack designs are reducing costs and improving durability. Companies like Bosch, Mitsubishi Heavy Industries, and Ceres Power are deploying scalable, modular SOFC systems with longer life cycles and faster ramp-up capabilities.

4. Demand for Distributed and Backup Power SOFCs are ideal for backup power in data centers, hospitals, and telecom infrastructure due to their low noise, low emissions, and minimal maintenance requirements. Their fuel flexibility ensures deployment in remote or off-grid areas, expanding their utility across regions with limited energy access.

Regional Insights: U.S. and Japan Lead Global Momentum

United States North America holds a substantial share of the SOFC market, led by major companies like Bloom Energy. The country is investing in hydrogen hubs and SOFC deployments for utility-scale and microgrid systems. Favorable tax credits and funding for energy resilience are further accelerating SOFC integration across public and private sectors.

Japan Japan is one of the world’s most aggressive adopters of SOFC technology. With a focus on energy security and net-zero goals, the country has launched initiatives to deploy millions of residential and commercial SOFC units. Companies such as Mitsubishi and Aisin are leading commercialization, while the government continues to subsidize installations and system development.

Market Segmentation and Technology Trends

Planar vs. Tubular SOFCs Planar solid oxide fuel cells dominate the market due to their modularity and lower manufacturing costs. Tubular designs are valued for their mechanical robustness but face challenges in scalability.

Stationary Applications Stationary SOFC systems remain the largest segment, accounting for more than 80% of the market. These are used in buildings, manufacturing plants, and district energy systems. Applications include backup power, grid balancing, and CHP.

Transport and Auxiliary Power Units (APUs) SOFCs are emerging in heavy-duty vehicles, marine transport, and aviation as auxiliary power sources. Their high energy density and quiet operation make them suitable for electrifying long-haul and industrial vehicles.

Portable and Remote Power Smaller SOFC units are being explored for military, camping, and disaster-recovery applications, especially where long-duration, off-grid energy is needed.

Get the Demo Full Report : https://www.datamintelligence.com/enquiry/solid-oxide-fuel-cell-market

Growth Opportunities

1. Hydrogen Integration and Reversible Systems SOFCs can run on hydrogen, and next-generation reversible SOFCs (rSOFCs) offer bidirectional functionality producing hydrogen when excess electricity is available and generating power when needed. This makes them ideal for future hydrogen grid integration.

2. Low-Temperature SOFC Development Companies are developing SOFCs that operate below 600°C, which reduces material costs and allows faster startup. This opens up new possibilities in transport and consumer electronics.

3. Marine and Defense Applications SOFC systems are being tested in naval vessels and defense infrastructure due to their stealth capabilities and independence from traditional fuel logistics.

4. Emerging Markets and Rural Electrification Regions in Southeast Asia, Africa, and South America are investing in decentralized energy solutions. SOFC systems provide clean, stable energy for off-grid villages and industrial operations.

Challenges and Constraints

High Capital Costs: While prices are falling, SOFC systems still carry high upfront costs due to materials and system integration.

Durability and Thermal Cycling: High operating temperatures lead to thermal stress. Innovation in stack materials and coatings is required for broader adoption.

Regulatory and Infrastructure Gaps: Deployment is constrained by a lack of uniform codes for hydrogen infrastructure and distributed generation.

Fuel Supply Chain: Access to affordable and clean hydrogen remains a bottleneck in many markets.

Conclusion

The global solid oxide fuel cell market is on a transformative path, aligning with the world’s urgent push toward clean and distributed energy. Governments, enterprises, and technology developers are now working together to scale up production, reduce costs, and expand SOFC applications across sectors.

With projected market values surpassing USD 20 billion by 2032, companies that innovate in stack design, fuel flexibility, and system integration will lead the next wave of sustainable power solutions. As the U.S. and Japan continue to drive research and commercialization, the SOFC industry is well-positioned to become a cornerstone of the global green energy future.

0 notes

Text

Wavelength Division Multiplexing Module Market: Expected to Reach USD 5.92 Bn by 2032

MARKET INSIGHTS

The global Wavelength Division Multiplexing Module Market size was valued at US$ 2.84 billion in 2024 and is projected to reach US$ 5.92 billion by 2032, at a CAGR of 11.3% during the forecast period 2025-2032. The U.S. accounted for 32% of the global market share in 2024, while China is expected to witness the fastest growth with a projected CAGR of 13.5% through 2032.

Wavelength Division Multiplexing (WDM) modules are optical communication components that enable multiple data streams to be transmitted simultaneously over a single fiber by using different wavelengths of laser light. These modules play a critical role in expanding network capacity without requiring additional fiber infrastructure. The technology is categorized into Coarse WDM (CWDM) and Dense WDM (DWDM), with applications spanning telecommunications, data centers, and enterprise networks.

The market growth is primarily driven by escalating data traffic demands, with global IP traffic projected to reach 4.8 zettabytes annually by 2026. The 1270nm-1310nm wavelength segment currently dominates with over 45% market share due to its cost-effectiveness in short-haul applications. Recent technological advancements include the development of compact, pluggable modules that support 400G and 800G transmission rates, with companies like Cisco and Huawei introducing AI-powered WDM solutions for enhanced network optimization. The competitive landscape features established players such as Nokia, Corning, and Infinera, who collectively held 58% of the market share in 2024 through innovative product portfolios and strategic partnerships with telecom operators.

MARKET DYNAMICS

MARKET DRIVERS

Exploding Demand for High-Bandwidth Connectivity Accelerates WDM Module Adoption

The global surge in data consumption, driven by 5G deployment, cloud computing, and IoT expansion, is fundamentally transforming network infrastructure requirements. Wavelength Division Multiplexing (WDM) modules have emerged as critical enablers for meeting this unprecedented bandwidth demand. Industry data indicates that global IP traffic is projected to grow at a compound annual growth rate exceeding 25% through 2030, with video streaming and enterprise cloud migration accounting for over 75% of this traffic. WDM technology allows network operators to scale capacity without costly fiber trenching by transmitting multiple data streams simultaneously over a single optical fiber. Recent tests have demonstrated commercial WDM systems delivering 800Gbps per wavelength, with terabit-capacity modules entering field trials. This scalability makes WDM solutions indispensable for telecom providers facing capital expenditure constraints.

Data Center Interconnect Boom Fuels Market Expansion

The rapid proliferation of hyperscale data centers and edge computing facilities has created an insatiable need for high-density interconnects. WDM modules are becoming the preferred solution for data center interconnects (DCI), with adoption rates increasing by approximately 40% year-over-year in major cloud regions. The technology’s ability to reduce fiber count by up to 80% while maintaining low latency has proven particularly valuable for hyperscalers operating campus-style deployments. Market analysis shows that WDM-based DCI solutions now account for over 60% of new installations in North America and Asia-Pacific regions. Recent product innovations such as pluggable coherent DWDM modules have further accelerated adoption by simplifying deployment in space-constrained data center environments.

Government Broadband Initiatives Create Favorable Market Conditions

National digital infrastructure programs worldwide are driving substantial investments in optical network upgrades. Numerous countries have allocated billions in funding for fiber optic network expansion, with WDM technology specified as a core component in over 70% of these initiatives. The technology’s ability to future-proof networks while minimizing physical infrastructure requirements aligns perfectly with public sector connectivity goals. Regulatory mandates for universal broadband access are further stimulating demand, particularly in rural and underserved areas where WDM solutions enable efficient network extension. These coordinated public-private partnerships are expected to sustain market growth through the decade, with particular strength in emerging economies undergoing digital transformation.

MARKET RESTRAINTS

Component Shortages and Supply Chain Disruptions Impede Market Growth

The WDM module market continues to face significant supply-side challenges, with lead times for critical components extending beyond 40 weeks in some cases. The industry’s reliance on specialized optical components manufactured by a concentrated supplier base has created vulnerabilities in the value chain. Recent geopolitical tensions and trade restrictions have exacerbated these issues, particularly affecting the availability of indium phosphide chips and precision optical filters. Manufacturers report that component scarcity has constrained production capacity despite strong demand, with some vendors implementing allocation strategies for high-demand products. This supply-demand imbalance has led to price volatility and extended delivery timelines, potentially delaying network upgrade projects across multiple sectors.

High Deployment Complexity Limits SMB Adoption

While large enterprises and telecom operators have readily adopted WDM technology, small and medium businesses face significant barriers to entry. The technical complexity of designing and maintaining WDM networks requires specialized expertise that is often cost-prohibitive for smaller organizations. Industry surveys indicate that nearly 65% of SMBs cite lack of in-house optical networking skills as the primary obstacle to WDM adoption, followed by concerns about interoperability with existing infrastructure. The requirement for trained personnel to configure wavelength plans and perform optical power budgeting creates additional operational challenges. These factors have constrained market penetration in the SMB segment, despite the clear economic benefits of WDM solutions for bandwidth-constrained organizations.

Intense Price Competition Squeezes Manufacturer Margins

The WDM module market has become increasingly competitive, with average selling prices declining approximately 12% annually despite advancing technology capabilities. This price erosion stems from fierce competition among manufacturers and the growing influence of hyperscale buyers negotiating volume discounts. While unit shipments continue to grow, profitability pressures have forced some vendors to exit certain product segments or consolidate operations. The commoditization of basic CWDM products has been particularly pronounced, with gross margins falling below 30% for many suppliers. This competitive environment creates challenges for sustaining R&D investment in next-generation technologies, potentially slowing the pace of innovation in the mid-term.

MARKET OPPORTUNITIES

Open Optical Networking Creates New Ecosystem Opportunities

The shift toward disaggregated optical networks presents a transformative opportunity for WDM module vendors. Open line system architectures, which decouple hardware from software, are gaining traction with operators seeking to avoid vendor lock-in. This transition has created demand for standardized WDM modules compatible with multi-vendor environments. Early adopters report 40-50% reductions in capital expenditures through open optical networking approaches. Module manufacturers that can deliver carrier-grade products with robust interoperability testing stand to capture significant market share as this trend accelerates. The emergence of plug-and-play modules with built-in intelligence for automated wavelength provisioning is particularly promising, reducing deployment complexity while maintaining performance.

Coherent Technology Migration Opens New Application Areas

Advancements in coherent WDM technology are enabling expansion into previously untapped market segments. The development of low-power, compact coherent modules has made the technology viable for metro and access network applications, not just long-haul routes. Industry trials have demonstrated coherent WDM successfully deployed in last-mile scenarios, potentially revolutionizing fiber deep architectures. This migration is supported by silicon photonics integration that reduces power consumption by up to 60% compared to traditional coherent implementations. Manufacturers investing in these miniaturized coherent solutions can capitalize on the growing need for high-performance connectivity across diverse network environments, from 5G xHaul to enterprise backbones.

Emerging Markets Present Untapped Growth Potential

The ongoing digital transformation in developing economies represents a significant expansion opportunity for WDM technology providers. As these regions upgrade legacy infrastructure to support growing internet penetration, demand for cost-effective bandwidth scaling solutions has intensified. Market intelligence indicates that WDM adoption in Southeast Asia and Latin America is growing at nearly twice the global average rate, driven by mobile operator network modernization programs. Local manufacturing initiatives and government incentives for telecom equipment production are further stimulating market growth. Vendors that can deliver ruggedized, maintenance-friendly WDM solutions tailored to emerging market operating conditions stand to benefit from this long-term growth trajectory.

MARKET CHALLENGES

Technology Standardization Issues Complicate Interoperability

The WDM module market faces persistent challenges related to technology standardization and interoperability. While industry groups have made progress in defining interface specifications, practical implementation often reveals compatibility issues between different vendors�� equipment. Recent network operator surveys indicate that nearly 35% of multi-vendor WDM deployments experience interoperability problems requiring costly workarounds. These challenges are particularly acute in coherent optical systems, where proprietary implementations of key technologies like probabilistic constellation shaping create vendor-specific performance characteristics. The resulting integration complexities increase total cost of ownership and can delay service rollout timelines, potentially slowing overall market growth.

Thermal Management Becomes Critical Performance Limiter

As WDM modules increase in density and capability, thermal dissipation has emerged as a significant design challenge. Next-generation modules packing more than 40 wavelengths into single-slot form factors generate substantial heat loads that can impair performance and reliability. Industry testing reveals that temperature-related issues account for approximately 25% of field failures in high-density WDM systems. The problem is particularly acute in data center environments where air cooling may be insufficient for thermal management. Manufacturers must invest in advanced packaging technologies and materials to address these thermal constraints while maintaining competitive module footprints and power budgets.

Skilled Workforce Shortage Threatens Implementation Capacity

The rapid expansion of WDM networks has exposed a critical shortage of qualified optical engineering talent. Industry analysis suggests the global shortfall of trained optical network specialists exceeds 50,000 professionals, with the gap widening annually. This talent crunch affects all market segments, from module manufacturing to field deployment and maintenance. Network operators report that 60% of WDM-related service delays stem from workforce limitations rather than equipment availability. The specialized knowledge required for wavelength planning, optical performance optimization, and fault isolation creates a steep learning curve for new entrants. Without concerted industry efforts to expand training programs and knowledge transfer initiatives, this skills gap could constrain market growth potential in coming years.

WAVELENGTH DIVISION MULTIPLEXING MODULE MARKET TRENDS

5G Network Expansion Driving Demand for Higher Bandwidth Solutions

The rapid global rollout of 5G infrastructure is accelerating demand for wavelength division multiplexing (WDM) modules, as telecom operators require fiber optic solutions that can handle exponential increases in data traffic. With 5G networks generating up to 10 times more traffic per cell site than 4G, WDM technology has become essential for optimizing existing fiber infrastructure instead of deploying costly new cabling. The 1270nm-1310nm segment shows particularly strong growth potential due to its compatibility with current network architectures, with projections indicating this wavelength range could capture over 35% of the market by 2032. This trend is reinforced by increasing investments in 5G globally, particularly in Asia where China accounts for nearly 60% of current 5G base stations worldwide.

Other Trends

Data Center Interconnectivity

Hyperscale data centers are increasingly adopting DWDM (Dense Wavelength Division Multiplexing) solutions to manage the massive data flows between facilities. As cloud computing continues its expansion with a projected 20% annual growth rate, data center operators require high-capacity optical networks that can support 400G and 800G transmission speeds. The WDM module market benefits significantly from this shift, with fiber-based interconnects becoming the standard for latency-sensitive applications like AI processing and financial transactions. Recent innovations in pluggable optics have made WDM solutions more accessible for data center applications, reducing power consumption by up to 40% compared to traditional implementations.

Emergence of Next-Generation Optical Networking Standards

The adoption of flexible grid technology is transforming WDM module capabilities, allowing dynamic allocation of bandwidth across optical channels. This development enables more efficient spectrum utilization and supports the evolution toward software-defined optical networks. Market leaders are increasingly integrating coherent detection technology into WDM modules, enhancing performance for long-haul transmissions critical for undersea cables and continental backbone networks. While these advancements present significant opportunities, they also require manufacturers to invest heavily in R&D—currently estimated at 15-20% of revenue for leading players—to maintain technological competitiveness in this rapidly evolving sector.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation and Strategic Expansion to Maintain Dominance

The global Wavelength Division Multiplexing (WDM) module market features a dynamic competitive landscape where established telecom giants and specialized optical solution providers coexist. Nokia and Cisco collectively accounted for over 25% of the global market share in 2024, leveraging their extensive telecommunications infrastructure and frequent product innovations. Both companies have recently expanded their WDM product lines to support 400G and beyond optical networks.

Meanwhile, Huawei continues to dominate the Asia-Pacific region with cost-effective solutions, while Fujitsu and ZTE have gained significant traction in emerging markets. These players differentiate themselves through customized wavelength solutions tailored for hyperscale data centers and 5G backhaul applications.

Specialized manufacturers such as Corning and CommScope maintain strong positions in the North American and European markets through continuous R&D investments. Corning’s recent development of compact, low-power consumption WDM modules has particularly strengthened its market position in energy-conscious data center applications.

The market has witnessed increased merger and acquisition activity, with larger players acquiring niche technology providers to expand their product portfolios. This trend is expected to intensify as demand grows for integrated optical networking solutions combining WDM with other technologies like coherent optics.

List of Key Wavelength Division Multiplexing Module Companies

Nokia (Finland)

Cisco Systems, Inc. (U.S.)

Huawei Technologies Co., Ltd. (China)

Fujitsu Limited (Japan)

ZTE Corporation (China)

Corning Incorporated (U.S.)

CommScope Holding Company, Inc. (U.S.)

ADVA Optical Networking (Germany)

Infinera Corporation (U.S.)

Fujikura Ltd. (Japan)

Lantronix, Inc. (U.S.)

Fiberdyne Labs (U.S.)

Segment Analysis:

By Type

1270nm-1310nm Segment Leads Due to Increasing Demand in Short-Range Optical Networks

The market is segmented based on wavelength range into:

1270nm-1310nm

1330nm-1450nm

1470nm-1610nm

By Application

Telecommunication & Networking Segment Dominates Owing to Rapid 5G Deployment

The market is segmented based on application into:

Telecommunication & Networking

Data Centers

Others

By End User

Enterprise Sector Leads Adoption for Efficient Bandwidth Management

The market is segmented based on end user into:

Telecom Service Providers

Data Center Operators

Enterprise Networks

Government & Defense

Others

By Technology

DWDM Technology Holds Major Share for Long-Haul Transmission

The market is segmented based on technology into:

Coarse WDM (CWDM)

Dense WDM (DWDM)

Wide WDM (WWDM)

Regional Analysis: Wavelength Division Multiplexing Module Market

North America The North American Wavelength Division Multiplexing (WDM) module market is driven by robust demand from hyperscale data centers and telecommunications networks upgrading to higher bandwidth capacities. The U.S. accounts for over 70% of regional market share, fueled by 5G deployments and cloud service expansions by major tech firms. While enterprise adoption is growing steadily, carrier networks remain the primary consumers. Regulatory pressures for energy-efficient networking solutions are accelerating the shift toward advanced WDM technologies, particularly dense wavelength division multiplexing (DWDM) systems. The market is characterized by strong R&D investments from established players like Cisco and Corning.

Europe Europe’s WDM module market benefits from extensive fiber optic deployments across EU member states and strict data sovereignty regulations driving localized data center growth. Germany and the U.K. lead adoption, with significant investments in metro and long-haul network upgrades. The region shows particular strength in coherent WDM solutions for high-speed backhaul applications. However, market growth faces temporary headwinds from economic uncertainties and supply chain realignments post-pandemic. European operators prioritize vendor diversification, creating opportunities for both western manufacturers and competitive Asian suppliers.

Asia-Pacific Asia-Pacific dominates global WDM module consumption, with China alone representing approximately 40% of worldwide demand. Explosive growth in mobile data traffic, government digital infrastructure programs, and thriving hyperscaler ecosystems propel market expansion. While Japan and South Korea focus on cutting-edge DWDM implementations, emerging markets are driving volume demand for cost-effective coarse WDM (CWDM) solutions. India’s market is growing at nearly 15% CAGR as it rapidly modernizes its national broadband network. The region benefits from concentrated manufacturing hubs but faces margin pressures from intense price competition among domestic suppliers.

South America South America’s WDM module adoption remains concentrated in Brazil, Argentina and Chile, primarily serving international connectivity hubs and financial sector requirements. Market growth is constrained by limited domestic fiber manufacturing capabilities and foreign currency volatility affecting capital expenditures. However, submarine cable landing stations and mobile operator network upgrades provide stable demand drivers. The region shows particular interest in modular, scalable WDM solutions that allow gradual capacity expansion – an approach that suits the cautious investment climate and phased infrastructure rollout strategies.

Middle East & Africa The Middle East demonstrates strong WDM module uptake focused on smart city initiatives and regional connectivity projects like the Gulf Cooperation Council’s fiber backbone. UAE and Saudi Arabia lead deployment, with significant investments in carrier-neutral data centers adopting wavelength-level interconnection services. In contrast, African adoption remains largely limited to undersea cable termination points and mobile fronthaul applications. While the market shows long-term potential, adoption barriers include limited technical expertise and reliance on international vendors for both equipment and maintenance support across most countries.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Wavelength Division Multiplexing Module markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 1.2 billion in 2024 and is projected to reach USD 2.8 billion by 2032, growing at a CAGR of 11.3%.

Segmentation Analysis: Detailed breakdown by product type (1270nm-1310nm, 1330nm-1450nm, 1470nm-1610nm), application (Telecommunication & Networking, Data Centers, Others), and end-user industry to identify high-growth segments.

Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific accounted for 42% market share in 2024.

Competitive Landscape: Profiles of 18 leading market participants including Cisco, Nokia, Huawei, and Infinera, covering their market share (top 5 players held 55% share in 2024), product portfolios, and strategic developments.

Technology Trends: Analysis of emerging innovations in DWDM, CWDM, and optical networking technologies, including integration with 5G infrastructure.

Market Drivers: Evaluation of key growth factors such as increasing bandwidth demand, data center expansion, and 5G deployment, along with challenges like supply chain constraints.

Stakeholder Analysis: Strategic insights for optical component manufacturers, network operators, system integrators, and investors.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/fieldbus-distributors-market-size-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/consumer-electronics-printed-circuit.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/metal-alloy-current-sensing-resistor.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/modular-hall-effect-sensors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/integrated-optic-chip-for-gyroscope.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/industrial-pulsed-fiber-laser-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/unipolar-transistor-market-strategic.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/zener-barrier-market-industry-growth.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/led-shunt-surge-protection-device.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/type-tested-assembly-tta-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/traffic-automatic-identification.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/one-time-fuse-market-how-industry.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/pbga-substrate-market-size-share-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/nfc-tag-chip-market-growth-potential-of.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/silver-nanosheets-market-objectives-and.html

0 notes

Text

SiC MOSFET Chips (Devices) and Module Market 2025

Silicon Carbide (SiC) MOSFET chips (devices) and modules are semiconductor components made from silicon carbide material. Compared to traditional silicon-based MOSFETs, SiC MOSFETs offer superior properties such as lower on-resistance, higher thermal conductivity, and reduced switching losses. These features make SiC MOSFETs highly suitable for high-frequency circuits, electric vehicles (EVs), renewable energy systems, industrial automation, and telecommunications applications.

Get more reports of this sample : https://www.intelmarketresearch.com/download-free-sample/639/sic-mosfet-chips-devices-and-module-market

Market Size & Growth Projections

The global SiC MOSFET chips (devices) and module market was valued at USD 540.9 million in 2022 and is projected to reach USD 2731.9 million by 2029, growing at a CAGR of 26.0% during the forecast period. The increasing adoption of electric vehicles and renewable energy solutions, coupled with advancements in semiconductor technology, is driving this growth. The demand for higher efficiency power electronics in industrial applications is also a significant contributor.

Key Market Drivers

Surge in Electric Vehicle Adoption: The rapid shift towards EVs is driving demand for SiC MOSFETs due to their superior efficiency in powertrain and charging applications.

Growing Renewable Energy Demand: SiC MOSFETs improve efficiency in solar inverters and wind power converters, significantly reducing energy losses.

High Performance & Energy Efficiency: Compared to silicon-based alternatives, SiC MOSFETs deliver better power density, thermal performance, and overall efficiency.

Industrial Automation & Power Electronics Expansion: Industries are integrating SiC MOSFETs in high-power applications such as motor drives, UPS, and power supplies.

Market Challenges & Restraints

High Manufacturing Costs: The production of SiC wafers is expensive, increasing the overall cost of SiC MOSFETs.

Complex Fabrication Process: SiC MOSFET manufacturing involves intricate and advanced processes, limiting large-scale production.

Limited Supply Chain & Market Consolidation: A few key players dominate the SiC MOSFET market, leading to supply chain constraints.

Opportunities for Growth

Expanding Applications in 5G & Aerospace: SiC MOSFETs are increasingly used in telecom infrastructure and satellite power systems.

Advancements in Manufacturing Technologies: The development of 6-inch and 8-inch SiC wafers will enhance production efficiency and reduce costs.

Rising Demand in Smart Grids & Power Infrastructure: SiC MOSFETs play a crucial role in modernizing energy distribution systems.

Regional Market Insights

North America

Strong demand due to the increasing adoption of EVs, 5G networks, and renewable energy solutions.

The United States leads the region, supported by a robust semiconductor industry and government incentives.

Europe

Germany dominates the European market, driven by its strong automotive and renewable energy sectors.

Government policies favoring energy-efficient technologies fuel market growth.

Asia-Pacific

China and Japan lead in SiC MOSFET production, accounting for a significant portion of global output.

The region’s booming EV and semiconductor markets are key growth drivers.

South America & Middle East-Africa

Brazil is the leading market in South America, with increasing investments in renewable energy and EV adoption.

Saudi Arabia and UAE are gradually adopting SiC MOSFETs in renewable energy projects.

Get more reports of this sample : https://www.intelmarketresearch.com/download-free-sample/639/sic-mosfet-chips-devices-and-module-market

Competitive Landscape

The SiC MOSFET market is highly competitive, with the top five companies holding approximately 80% market share. Key players include:

Infineon Technologies

Wolfspeed (Cree)

ROHM Semiconductor

STMicroelectronics

ON Semiconductor

Mitsubishi Electric

These companies are investing in manufacturing expansion, product development, and strategic partnerships to strengthen their market position.

Market Segmentation (by Application)

Electric Vehicles (EVs) and Hybrid Vehicles: SiC MOSFETs improve battery performance and efficiency.

Renewable Energy Systems: Used in solar inverters, wind turbines, and power converters.

Industrial Power Electronics: Deployed in motor drives, UPS, and power grid applications.

5G & Telecommunications: Enhances power efficiency in base stations and network equipment.

Aerospace & Defense: Integrated into satellites, aircraft power systems, and radar electronics.

Market Segmentation (by Type)

SiC MOSFET Chips/Devices: Used in standalone power conversion applications.

SiC MOSFET Modules: Integrated solutions for high-power industrial applications.

Key Developments & Innovations

June 2021: Infineon Technologies acquired Cypress Semiconductor to expand its automotive and IoT portfolio.

May 2021: Wolfspeed expanded SiC MOSFET production for EV and renewable energy applications.

February 2021: ON Semiconductor introduced high-voltage SiC MOSFETs for renewable energy.

January 2021: STMicroelectronics launched a SiC MOSFET power module for EVs.

October 2021: ROHM Semiconductor developed a low on-resistance SiC MOSFET chip for higher efficiency.

Geographic Segmentation

Asia-Pacific: Largest market due to China, Japan, and South Korea’s semiconductor and EV industries.

North America: Strong growth in EVs and 5G infrastructure.

Europe: Germany, France, and the UK lead in automotive and energy applications.

Frequently Asked Questions (FAQs) :

▶ What is the current market size of the SiC MOSFET market?

A: The market was valued at USD 540.9 million in 2022 and is expected to reach USD 2731.9 million by 2029.

▶ Which are the key companies in the SiC MOSFET market?

A: Leading players include Infineon Technologies, Wolfspeed, Rohm Semiconductor, STMicroelectronics, ON Semiconductor, and Mitsubishi Electric.

▶ What are the key growth drivers in the SiC MOSFET market?

A: Major growth factors include EV adoption, high-efficiency power electronics, and renewable energy expansion.

▶ Which regions dominate the SiC MOSFET market?

A: Asia-Pacific leads the market, followed by North America and Europe.

▶ What are the emerging trends in the SiC MOSFET market?

A: Trends include 8-inch wafer production, high-voltage SiC MOSFETs, and aerospace/industrial applications.

Get more reports of this sample : https://www.intelmarketresearch.com/download-free-sample/639/sic-mosfet-chips-devices-and-module-market

0 notes

Text

Roam is transforming the global telecommunications landscape by offering a decentralized platform that delivers free eSIM and WiFi connectivity in over 190 countries. Designed to eliminate roaming fees and lower barriers to international mobile data access, Roam combines blockchain incentives with community-powered infrastructure to provide an innovative solution for users worldwide.

The platform operates through its dedicated mobile app, Roam: Free Global eSIM and WiFi, which is available for download on Android at https://play.google.com/store/apps/details?id=com.dapp.metablox and on iOS at https://apps.apple.com/app/roam-free-global-esim-and-wifi/id6475934064. Once installed, users can activate an eSIM directly within the app or connect to nearby community-contributed WiFi hotspots, eliminating the need for physical SIM cards or expensive international data plans. With real-time access and automated configuration, Roam offers a seamless onboarding experience for users who need reliable data anywhere in the world.

One of Roam’s most distinctive features is its decentralized WiFi-sharing network, which allows individuals and businesses to contribute unused bandwidth. In return, they are rewarded through a points-based system known as Roam Points. These points are awarded for actions such as WiFi check-ins, daily usage, and successful referrals. Users can redeem Roam Points for additional data or other in-app utilities, making the platform self-sustaining and community-driven.

Supporting this system is $ROAM, the platform’s Solana-based utility token. $ROAM enables various functions across the network including staking, node rewards, and future governance participation. Token holders may earn rewards by operating Roam Miners—dedicated devices that help expand network coverage—and by engaging in staking protocols that promote token utility and network stability. $ROAM is currently listed on major exchanges such as MEXC, Uniswap, and Binance Alpha, giving it high accessibility and liquidity in the broader crypto economy.

Roam also incentivizes user growth through a referral program. New users who sign up using the referral code 71141625 receive bonus Roam Points, contributing to faster network expansion through peer-to-peer promotion. This model aligns with the platform’s mission to grow organically while reducing reliance on centralized marketing efforts.

By emphasizing user control, decentralization, and borderless access, Roam addresses long-standing inefficiencies in the global telecom industry. Traditional mobile networks often charge exorbitant roaming fees and offer limited interoperability between regions. Roam’s open infrastructure model challenges this paradigm, offering a scalable, cost-effective alternative driven by community participation.

Currently, the platform supports eSIM and WiFi services in more than 190 countries, with expanding infrastructure and increasing adoption. This makes Roam especially attractive to international travelers, digital nomads, remote workers, and populations in emerging markets where traditional mobile services may be unreliable or unaffordable.

Those interested in learning more or joining the network can visit https://weroam.xyz/join_us. For ongoing updates, the platform actively shares news through its Twitter account @weRoamxyz.

Roam’s approach represents a significant evolution in the connectivity space—where open access, token incentives, and decentralized systems converge to deliver global mobile internet without borders.

1 note

·

View note

Text

Switchgear Market Growth Driven by Renewable Energy and Infrastructure Expansion

Market Overview

The switchgear market is on a growth trajectory as global energy infrastructure evolves to meet rising electricity demand and the increasing integration of renewable energy. As modernization of power grids gains momentum, the demand for advanced and efficient switchgear solutions is seeing consistent growth.

The switchgear market size is projected to reach USD 174.38 billion by 2030 from an estimated USD 129.70 billion in 2025, growing at a CAGR of 6.1% during the forecast period (2025–2030).

Key Trends

Smart Grid Integration Accelerates Switchgear Demand The adoption of smart grid systems globally is contributing to the expansion of the switchgear industry. These systems require modern, intelligent switchgear that supports automation, real-time monitoring, and grid flexibility.

Rise in Renewable Energy Installations With countries shifting toward sustainable energy sources, the deployment of wind and solar power installations is creating additional demand for medium and high-voltage switchgear. These solutions are critical for integrating renewables into the grid and ensuring safe power distribution.

Urbanization and Infrastructure Development Rapid urban development, especially in Asia-Pacific and the Middle East, is increasing the need for reliable electrical distribution networks. This is directly influencing the switchgear market size as both utility and commercial sectors invest in upgrading power systems.

Industrial Automation and Electrification Industries are increasingly embracing automation and digitization, driving demand for compact and efficient switchgear to manage electrical loads effectively. Low-voltage switchgear, in particular, is gaining popularity in manufacturing and processing facilities.

Technological Advancements in GIS and AIS Innovations in gas-insulated switchgear (GIS) and air-insulated switchgear (AIS) are enhancing operational efficiency, reducing footprint, and enabling easier maintenance. These advancements are positively impacting the switchgear market trends globally.

Challenges

Despite strong growth indicators, the switchgear market faces several challenges. High initial installation costs, especially for advanced GIS systems, act as a barrier for smaller utilities and developing regions. Additionally, supply chain disruptions and the volatility in raw material prices can affect production and delivery timelines. Environmental concerns related to SF6 gas used in GIS are also leading to regulatory pressures, pushing manufacturers to seek greener alternatives.

Conclusion

The switchgear industry is undergoing a transformative phase, driven by global trends in electrification, sustainability, and technological innovation. The switchgear market analysis indicates robust opportunities, especially in developing economies, where infrastructure development and industrialization are on the rise. As revealed in the switchgear industry report, market participants are investing in R&D and digital solutions to stay ahead in a competitive landscape. With the switchgear market share expanding steadily, this sector is poised to play a pivotal role in enabling a more reliable, efficient, and future-ready power distribution ecosystem.

Other Related Reports: 3D Printing Market

Telecom Cloud Market

Chiller Market

Paper Straw Market

#Switchgear Market#Switchgear Market Size#Switchgear Market Share#Switchgear Market Trends#Switchgear Market Analysis#Switchgear Industry

0 notes

Text

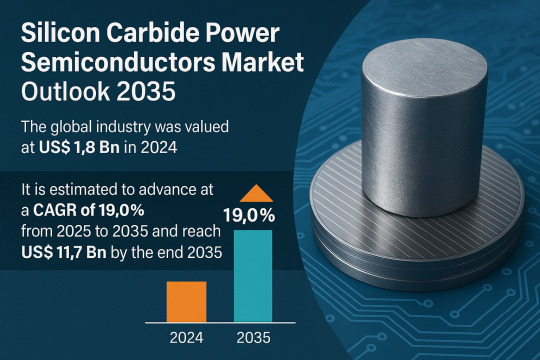

Silicon Carbide Market Soars with Demand for High-Efficiency Power Electronics

The global silicon carbide (SiC) power semiconductors market is witnessing a period of rapid transformation, powered by robust growth in electric vehicles (EVs), renewable energy infrastructure, and next-generation industrial automation. Valued at US$ 1.8 billion in 2024, the market is projected to grow at an impressive CAGR of 19.0% between 2025 and 2035, reaching a valuation of US$ 11.7 billion by the end of the forecast period.

Market Overview

The silicon carbide power semiconductors market has emerged as a cornerstone of modern energy and mobility solutions. SiC devices are increasingly replacing traditional silicon-based semiconductors due to their superior electrical efficiency, higher voltage resistance, and capability to function under high temperatures. These features make them indispensable in demanding applications such as electric vehicle powertrains, solar inverters, industrial motor drives, and telecom equipment.

Market Drivers & Trends

Two major forces are driving the market’s ascent:

The EV Boom: The global electric vehicle industry is projected to expand from US$ 255.5 Bn in 2023 to over US$ 2,100 Bn by 2033. This surge is significantly boosting demand for SiC power semiconductors, especially in high-efficiency traction inverters, onboard chargers, and battery management systems.

Fast-Charging Demand: With consumer preference leaning toward rapid EV charging, SiC devices are gaining ground due to their ability to handle high voltages and fast-switching frequencies. Their adoption improves power density while reducing heat losses, enabling compact and more efficient charger designs.

Latest Market Trends

MOSFETs Leading the Charge: Among product types, SiC-based MOSFETs are gaining the most traction, holding a 37.28% share in 2024 and projected to grow at 19.9% CAGR. These devices are essential for modern power electronics, offering unmatched efficiency and speed.

Miniaturization & Integration: Manufacturers are emphasizing the development of smaller, integrated SiC solutions to meet the spatial and thermal management needs of EVs, renewable systems, and consumer electronics.

Key Players and Industry Leaders

Prominent players driving innovation in the SiC market include:

STMicroelectronics N.V.

Infineon Technologies AG

WOLFSPEED, INC.

ON Semiconductor Corp

Mitsubishi Electric Corporation

GeneSiC Semiconductor Inc.

Analog Devices, Inc.

Littelfuse, Inc.

ROHM Co. Ltd

Semikron Danfoss

These companies are investing heavily in R&D and strategic partnerships to expand their product portfolios and global market footprint.

Recent Developments

STMicroelectronics (September 2024) launched its fourth-generation SiC MOSFET technology, setting new benchmarks in energy efficiency and robustness, especially for EV traction inverters.

Onsemi (July 2024) introduced the EliteSiC M3e MOSFET series, which delivers improved performance and reliability, ideal for electric powertrain and fast-charging infrastructure.

Market Opportunities

The global push toward decarbonization is opening vast opportunities for SiC power semiconductors:

EV Infrastructure Expansion: As governments invest in high-speed charging networks, SiC-based chargers and converters are becoming essential.

Smart Grids and Renewable Integration: SiC devices enable efficient power management in smart grids and solar inverters, making them crucial for renewable energy growth.

Industrial Automation and Robotics: Demand for precision control and high-performance motor drives is increasing the use of SiC semiconductors in advanced manufacturing settings.

Access important conclusions and data points from our Report in this sample – https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=86467

Future Outlook

The silicon carbide power semiconductors market is poised for transformative growth through 2035. As the world shifts toward sustainable energy and transportation systems, SiC devices will be central to enabling this change.

Government initiatives promoting EV adoption, combined with energy efficiency regulations, are expected to further boost market penetration across both developed and emerging economies. Advances in SiC manufacturing and packaging technologies will also help reduce costs, making them more accessible for mass-market applications.

Market Segmentation

By Product Type:

Diode

Power Module

MOSFETs (Leading)

Others

By Voltage:

Below 600V

601V – 1000V

1001V – 1500V

Above 1500V

By End-use Industry:

Automotive & Transportation (including EV Powertrains and BMS)

Aerospace & Defense

Consumer Electronics

IT & Telecommunication

Industrial Automation

Others (Healthcare, Utilities, etc.)

Regional Insights

East Asia dominates the global market with a 43.3% share in 2024 and is projected to grow at a CAGR of 17.6% through 2035. Countries like China, Japan, and South Korea are investing heavily in semiconductor fabrication, EV manufacturing, and renewable energy integration.

The region benefits from:

Strong government support for green technologies

Expansive R&D infrastructure

A growing domestic EV market

Established semiconductor supply chains

Meanwhile, North America and Western Europe are also experiencing significant growth, spurred by electrification programs and renewable energy mandates.

Why Buy This Report?

This comprehensive silicon carbide power semiconductors market report offers:

Detailed market size forecasts from 2025 to 2035

Insights on key drivers, trends, and challenges

Competitive landscape with profiles of major and emerging players

Segment-wise and regional analysis

Information on technological advancements and R&D focus areas

Strategic recommendations for stakeholders and investors

It is an essential resource for industry professionals, market analysts, policy makers, and anyone interested in the future of high-performance power electronics.

Frequently Asked Questions (FAQs)

Q1. What is the projected market value of the SiC power semiconductors market by 2035? A1. The market is forecasted to reach US$ 11.7 Bn by 2035.

Q2. What is the compound annual growth rate (CAGR) from 2025 to 2035? A2. The market is projected to grow at a CAGR of 19.0%.

Q3. Which product segment leads the market? A3. The MOSFETs segment is leading the market due to its high-speed switching and energy efficiency.

Q4. What are the major market drivers? A4. Growing demand for electric vehicles, fast-charging infrastructure, and renewable energy solutions are key growth drivers.

Q5. Which region holds the largest market share? A5. East Asia leads the global SiC power semiconductors market with a 43.3% share in 2024.

Q6. Who are the key players in the market? A6. STMicroelectronics, Infineon, WOLFSPEED, ON Semiconductor, Mitsubishi Electric, and others.

Q7. What are some recent innovations in the industry? A7. STMicroelectronics' 4th-gen SiC MOSFET and Onsemi’s EliteSiC M3e MOSFET are notable innovations enhancing performance and cost-efficiency.

0 notes

Text

Conversational AI Market Size, Share, Trends, Demand, Future Growth, Challenges and Competitive Analysis

Executive Summary Conversational AI Market Market :

Market research analysis carried out in this Conversational AI Market. Market report imparts its own benefits and advantages that will support to grow your business whether it is small or large size. The report gives several insights that will help to take your business in the right direction. Market research analysis conducted in this Conversational AI Market Market report is a powerful method that gives answers to many of your business challenges more quickly. Many professionals and businessmen rely on such syndicated market research report which acts as a go-to solution for them. Conversational AI Market Market research report save hours of time as well as add credibility to the work done.

In this fast-paced industry, market research or secondary research provided in this Conversational AI Market Market report is the best way to collect information quickly. The market research analysis of this report is carried out with the reliable knowledge of what the market expects, what already exists in the market, the competitive environment, and what steps to take to outshine the competition. Furthermore, market research report help to validate information gathered through primary sources. Such Conversational AI Market Market research report guide professionals for changes and offer them ways to justify what third parties say so that they are not prejudiced.